Crypto assets are still not a part of the asset allocation of institutional investors such as pension funds. In Switzerland the pension funds invest only in traditional assets, but it could be a good time to explore the inclusion of Crypto assets in their asset allocation.

Crypto assets – Low correlation – Diversification

Modern portfolio theory looks at an investment by its impact of on expected portfolio’s risk and return. A positive impact is achieved by assets that have beneficial attributes such as a desirably low correlation to other assets. This attribute plays not only a key role in its positive risk-reward contribution to portfolios, but to its potential acceptance as an asset class.

By calculating the efficient frontier with an increasing Bitcoin allocation of the traditional asset universe better risk-return portfolios measured by the Sharpe ratio are achieved (SEBA 2021).

Knowing about this benefit, even with a small allocation into Crypto assets, the question remains why institutional investors are not yet considering an allocation into Crypot assets? There may be still a lot of questions to be answered regarding regulation, risk, acceptance etc. but one question that can be addressed easily is “Where exactly do Crypto assets fit in a portfolio of institutional investors?”.

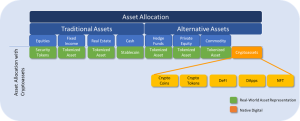

Crypto Assets – Where do they belong in the asset allocation?

The traditional asset allocation (on a very generic overview) is implemented via equities, fixed income, real estate, and alternative assets (hedge funds, private equity, commodities).

Source: Own illustration.

One may easily allocate the Crypto asset in the alternative asset space but that would not consider the specific attributes that Crypto assets have regarding:

1. Real-world representation:

A main differentiation attribution of Crypto assets is the real-word representation of an asset. The representation in a digital form of the asset can be made for tangible assets, like securities, precious metals, mineral resources, real estate, works of art, or intangible assets, like licenses, rights, graphics or documents (Ankenbrand et al. 2020). Crypto assets that do not have real-world underlying as a collateral are native digital assets such as Bitcoin or Ether.

2. Risk:

BIS (2021) states that “a Crypto asset that provides equivalent economic functions and poses the same risks compared with a “traditional asset” should be subject to the same capital, liquidity and other requirements as the traditional asset.” This is from a regulatory perspective important as this allows a similar treatment of the risk like the real-world asset represented as a Crypto asset. Examples for this category are security tokens, stable coins or any tokenized real-world asset.

3. Valuation:

From a valuation perspective, the question arises on how the security tokens and tokenized assets are valued. Sygnum (2021) sees no difference in the valuation of the real-world asset and its representation in digital form such as a security token or a tokenized asset.

In a portfolio context this translates into the fact that irrespective of the form of an asset, i.e. if it is a real-world asset or its digital representation it will be treated the same way.

Furthermore, as the main asset categories can be replicated by security tokens and tokenized assets the remaining category would be the alternative asset space as the below figure shows.

Source: Own illustration.

Conclusion

The emerging nature of native digital Crypto assets show a hedge fund or private equity risk/return structure and hence the classification as an alternative asset seems to be (at least from today’s perspective) correct.

This framework allows investors to correctly allocate the Crypto assets to the relevant asset category. This allows a correct handling of the risk/return attribution to the total portfolio performance.