Today’s financial services rely on dominant central institutions. For example, in Switzerland we only have one large public securities exchange, two dominating payment systems and five banks deemed “too big to fail”. Defi applications are, in essence, applications run on blockchains performing financial services, such as lending or trading, without reliance on an intermediary. Consequently, once deployed, these applications act autonomously and are rule-based. The underlying blockchain ensures that these rules are transparent, encrypted and irreversible, creating the trust needed to interact with them. Defi is still in its infancy but its use rocketed in 2020 and currently has USD 66 billions invested (Total Value Locked). This is a drop in the ocean compared to the USD 34 trillion global financial assets under management, but the 25x growth of Defi investments in one year hints that something bigger is brewing. Defi has the potential to create more efficient, innovative and client centric financial services, while still providing a role for intermediaries.

Financial services are not perceived as efficient due to high fixed costs, prudent risk management and cumbersome client experiences. Running a decentralised and automated service removes overhead costs in areas such as reconciliation between intermediaries (banks run whole units on verifying data) and reduces administration efforts. Defi’s transparent governance models encourage cost discipline for administration and product development. Moreover, removing intermediaries decreases counter-party risk and each % risk reduction results in $ saved.

Defi applications demonstrated their resilience impressively during the latest crypto down-turn by having no major outages. In contrast, after the last financial crisis, governments across the globe had to step in, as banks were not willing to lend to each other anymore.

Additionally, programmable financial services create innovative business models. Indeed, Defi applications are highly speculative, and are vulnerable to hacks and scams, with nearly no regulatory oversight. However, these open, fast-paced and well-funded ecosystems produce what might be missing in financial services: true innovation. Defi is a sandbox, small enough that failures are not existential threats to the economy, but large enough to provide proof for new successful concepts. Two samples of promising innovations are

- Decentralised exchanges / Liquidity pools

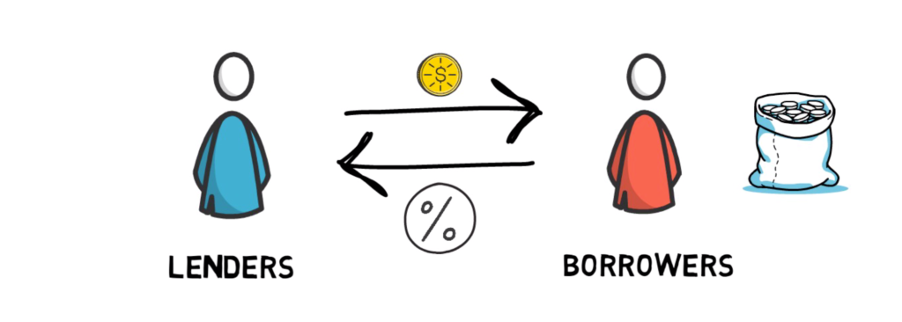

Illustration by finematics.com - Lending protocols

Illustration by finematics.com

I believe that such Defi concepts will converge over time with traditional financial services.

Lastly, the compelling new user experience will increase client interest in investing. Crypto and related offerings have significantly lowered the barrier to access financial services and even make it fun. You only need a free wallet application and some crypto tokens to get started. Additionally, the user experience is characterised by full transparency (fees, use of funds etc.), real-time transactions and data, 24/7 trading, new investment possibilities (e.g. staking, simplified lending) and easy access to participation (e.g. voting, funding). This will set a new benchmark and influence what investors expect from traditional financial services.

Defi seems to be here to stay but there are still hurdles to wider adoption such as complexity, new risks and scalability. While access is easy and returns high, investing in Defi can still be complex. Investors need to be tech-savvy to execute transactions and equipped with financial know-how to assess investment risks.

On top of the already highly speculative crypto market, Defi applications come with new economic (e.g. rug pulls) and technical risks (e.g. coding errors, hacks). Also, the lack of clear regulation exposes all participants to compliance risks. Reducing these threats will need new regulations, technological improvements and trustworthy key players.

Increasing transaction speed while keeping security and decentralisation is a constant blockchain dilemma limiting scalability. Defi applications have clogged the Ethereum network and raised transaction fees (“gas”) so high that smaller transactions are not economical anymore. The Ethereum 2.0 change to a Proof of Stake validation will address some scalability issues.

In conclusion, although the possibility of spectacular returns are what attract most investors today, when you look closer, it is the opportunity to re-invent finance that really stands out. Many new investors attracted to Defi will likely turn to professionals to help navigate these risks and complexity, hence creating new business opportunities for bold financial intermediaries.

Further readings:

https://future.a16z.com/cryptos-fourth-wave-defi-poised-for-breakthrough/

https://medium.com/racecapital/defi-infrastructure-101-overview-market-landscape-78e096a85834

https://www.economist.com/special-report/2021/05/06/a-future-with-fewer-banks