25. November 2018

Core+: A suitable investment style in the current environment

Core real estate strategies should continue to provide investors with solid but. In particular it is important to choose a suitable investment style. But how to allocate money among investment styles? Sven Schaltegger and Zoltan Szelyes describe in the following article the main three investment styles with foccussing on Core+ in the current environment.

Sven Schaltegger, Director Private Equity Real Estate at Credit Suisse and Zoltan Szelyes, Head of Global Research at Credit Suisse

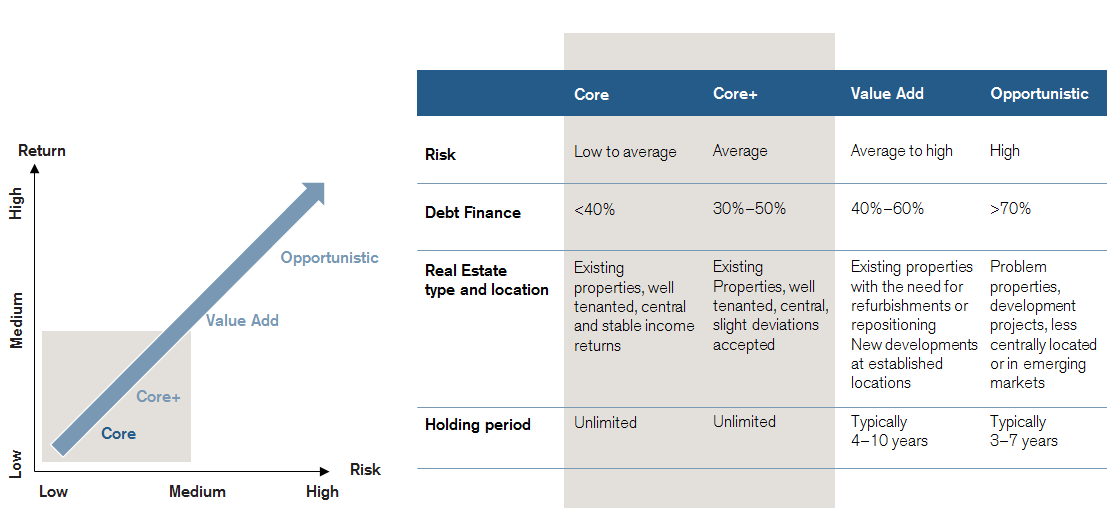

Investment strategies can be categorized in three main styles: Core, value-add and opportunistic. Illustration 1 highlights some key features of each strategy and shows that risk and return increase by moving from one to the next strategy.

Core: The backbone of any real estate allocation

“Core” describes investment strategies that focus on limiting risk and achieving stable and relatively predictable mid to high-single digit returns. The return is almost exclusively derived from rental income from existing stabilized[1] buildings. These strategies are typically limited to investments in established micro locations, such as central business districts for office properties. They are typically characterized by relatively long weighted-average unexpired lease terms (WAULTs) and rely on a diversified base of high-quality tenants that encompasses firms of good covenant strength from different industries.

While total returns for core strategies are not only comprised of net rental income but are influenced by changes in the respective property’s valuation (for instance as a consequence of changes in interest rates, demand-supply imbalances or idiosyncratic reasons) the lion’s share of returns of a core investment should come from income. Core strategies have the lowest volatility, partly because financial leverage is usually limited to 40% or less but is oftentimes considerably lower than that or even non-existent.

Value-add: Asset management strategies and market recovery plays

Value-add strategies typically aim to achieve returns in the low teens and allow for higher degrees of risk. Compared to core a considerably higher proportion of the return is expected to come from capital appreciation. The leverage applied is also substantially higher than for core and it is not unusual to see LTV ratios of up to 60% in value-add deals[2]. Typically, value-add funds invest in either buildings that have vacancies of up to 50% or are located in secondary micro or macro locations. In Germany this is mostly known as “ABBA” strategy: investments in A-quality properties in B locations or B-quality properties in A locations. The source of the value add returns can be pure asset management strategies such as creating a better tenant mix (retail), optimizing floor plans, improve the overall appearance, reconfigure a single tenant property to a multi-tenant asset (office) or leasing up existing vacancy. Ideally, value-add strategies are pursued in improving markets, as an improvement in the rental markets or yield compression helps to achieve the higher target returns. As holding periods are usually limited, a viable exit strategy and a liquid exit market, ideally with many core buyers, is key

Opportunistic: Higher return and risk strategies

Opportunistic strategies target IRRs greater than 15% and, in some cases, even above 20%. Opportunistic strategies include a range of sub-strategies; i) the most common one involves making profound physical changes to an existing building such as an extensive refurbishment (during which the building is vacant and, thus, generates no or only little cash flow), a change of use of a the property – for instance a conversion from office to residential use – or an outright development project. ii) Being able to buy an opportunistic deal relatively cheaply and preferably below replacement cost is a key part of the strategy. Reasons for an attractive acquisition price vary ranging from pro-active deal sourcing through a strong network, assessing risks differently than competing buyers to buying from distressed sellers and / or benefitting from better financing terms. iii)The re-positioning of the building to a higher use results in a stronger cash flow from the building which should be reflected in a higher valuation, an effect sometimes referred to as ‘yield shift’. iv) Another opportunistic strategy focuses less on the building itself but much more on how it is financed: properties with a distressed financing structure or whose owners are in financial distress can be attractive opportunities for financially savvy and cash-rich investors. In some cases investors get ownership to a property by buying debt which is then converted to equity. V) Opportunistic strategies can also include investments in emerging markets, typically associated with less transparency and less political stability leading to more volatile rents and, accordingly, more volatile real estate prices. Lastly, in case of very large investors, leveraged buyouts or public-to-private transactions of undervalued listed real estate companies can be an attractive opportunistic strategy as well. In most cases opportunistic investments are highly leveraged with LTVs of up to 65% or even 80%.

To sum up, both value-add and opportunistic strategies generally look for opportunities to acquire properties at attractive prices whose values can be enhanced through one of the afore-mentioned strategies. The last step is then to successfully exit the stabilized property, in many cases to a core investor. Before committing to a value-add or opportunistic fund – both of which are usually structured as closed-end, limit life vehicles – investors should make themselves familiar with a manager’s track record relevant to the proposed strategy and examine whether the people responsible for a manager’s past performance will be the ones implementing the new fund’s strategy. Given the elevated debt levels these funds operate with, investors should also ensure that the fund’s incentive structure does not lead the manager to take excessive financing risks. Since value-add and opportunistic funds do not usually provide for any liquidity during their term, investors should scrutinize the proposed fund and the respective manager before an investment.

[1] The term “stabilized” in this context refers to a high level of occupancy relative to the respective submarket and sector, typically 90-95%. Additionally, a stabilized building requires no or only limited capital expenditure to operate.

[2] Compared to the situation preceding the global financial crisis (“GFC”) it is, however, very uncommon in today’s market to see leverage and “strategies” such as early re-payment of investors’ equity by re-financing transactions as a distinct driver of return.

Wollen Sie mehr erfahren über die verschiedenen Investmentstyles und was die Vorteile von Core+ sein können?

Das Buch Indirect Real Estate Strategies mit dem gesamten Artikel können Sie hier beziehen.

Die Immobilienkonferenz „Indirekte Immobilienanlagen im In- und Ausland“ als Nachfolge zu dem Buch Indirect Real Estate Strategie ist bereits für das Jahr 2019 lanciert. Merken Sie sich jetzt schon Donnerstag, den 19. September 2019 vor!

Für Rückfragen steht Ihnen Prof. Dr. John Davidson gerne zur Verfügung.

Das könnte Sie ebenfalls interessieren:

Entdecken Sie die Welt des Immobilienmanagements und erfahren Sie alles Wissenswerte rund um den MAS Immobilienmanagement und andere Angebote zum Thema Immobilien. Gerne beantworten Ihnen Prof. Dr. Markus Schmidiger und Prof. Dr. John Davidson vom IFZ Ihre Fragen.

Kommentare

1 Kommentare

John

25. November 2018

Richtige Strategie für viele Schweizer PKs welche im Aufbau eines internationalen Portfolios sind!

Danke für Ihren Kommentar, wir prüfen dies gerne.